Carried interest and co-investment plans have long been central pillars

of compensation for investment professionals in private equity (PE) and alternative asset management. Stricter regulations, a competitive job market, and a growing emphasis on company values have forced significant change in both the market and the plans themselves. Private Equity firms now have to adjust to keep pace, and we are starting to see innovation and experimentation in an area that has traditionally been conservative in its approach.

Evolving PE Comp Trends (2019–2025)

- CARRIED INTEREST

Shorter vesting and crystallisation periods: Funds are moving away from traditional 8-10 year carry vehicles toward faster vesting, more frequent crystallisation, and deal-by-deal carry

in some strategies (especially in growth equity or sector-focused funds). - Retention enhancements: Many firms are now incorporating retention hooks, e.g., forfeiture or clawback clauses if individuals exit early or underperform.

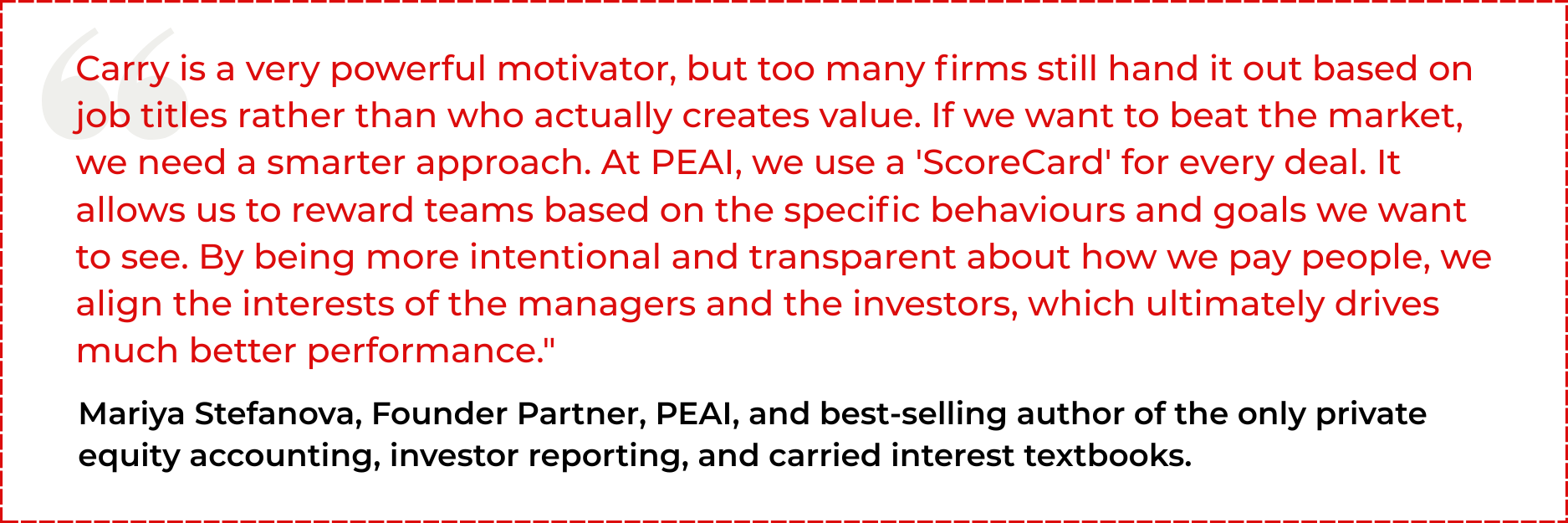

- Team-based allocations: More carry pools are being designed to reward the success of the team, not just seniority, possibly reflecting a push for broader cultural cohesion.

- CO-INVESTMENT PLANS

More accessible: Co-investment, once

only for top executives, is now available

to more employees, though with limits

on amount and leverage. - Streamlined structure: Automated and tech-enabled co-investment platforms

are the norm, helping firms manage large groups of co-investors more efficiently. - Risk mitigation: Some funds now allow for back-leverage facilities or offer downside protection in co-investments to encourage participation among more junior staff.

PE Equity Alternatives

Private equity firms face new competition from other long-term incentive plans, especially as tech and growth equity firms blur traditional industry lines. Because vesting periods are also becoming shorter and stranger, PE has had to adapt.

Emerging Competing Models

Phantom equity and synthetic carry: Common in asset-light or new platforms without an existing carry pool, they simulate economic exposure without actual equity ownership, though they often have less

favorable tax implications.

GP stakes and long-term equity grants:

Some firms are now offering equity in the management company itself, or direct profit-sharing from GP stakes, providing long-term alignment.

Annualized equity bonuses:

In response to carry’s long tail, firms (especially in EMEA) are experimenting with annual performance-linked equity grants to drive near-term motivation.

Examining Management Incentive Plans (MIPs)

The Problem with MIPs

PE and VC-backed organisations are now seeing a notable evolution in the structuring of their MIPs. Once considered a key attraction for executive talent, MIPs are now widely viewed as either inaccessible or as “phantom equity” with little real value unless a distant and uncertain exit occurs.

PE / VC-backed firms had also often rolled out quota-based commissions with multi-layered accelerators, retention hooks, and company-wide EBITDA gates. These were topped off with a MIP tied to equity value at exit. But the outcome was a structure so complex that even senior executives struggled to model their own reward potential, which therefore made them feel intangible.

Additionally, many PE-backed firms have high entry valuations and aggressive IRR or MOIC targets built into their MIPs. These may have made sense in a low-interest, high-growth world, but in today’s environment, with economic volatility the norm, many MIPs are structurally “underwater” requiring a minimum 2x–3x value creation to generate any real return.

Revolutionising MIPs

MIP’s are evolving to hybrid incentive models with cash now, equity later.

- Short-term cash performance bonuses are increasingly commonplace and are linked to annual business performance (based on bookings, margin or NRR)

- Retention bonuses or synthetic equity with quarterly or annual vesting

- Smaller, more transparent equity grants tied to milestone triggers

Forward-thinking investment funds are even now offering select leaders a share in the profits from specific deals, much like a synthetic form of carried interest. Instead of typical MIPs, some leaders receive additional performance-based payouts if they achieve a measurable increase in revenue or margin that directly boosts their company’s value.

A clear example of this was in 2018, when TA Associates provided the management team at Speedcast with incremental performance equity tranches: a 10% base grant plus additional tranches up to 20% at different return thresholds (e.g.: 1.5x, 2.0x, 2.5x, 3.0x MOIC). This gave them increasing exposure to value creation that was directly tied to their performance.

The Rise of Secondaries and Continuation Funds

In the past few years, traditional PE exit channels such as IPOs and strategic M&As have noticeably slowed down, leaving sponsors with fewer opportunities to realise value and return capital to investors.

As a result, secondary market transactions including continuation funds have surged.In 2025, global secondary deal volumes hit all-time highs. Continuation vehicles now make up a growing portion of total sponsor exits, as firms choose to hold onto their high-performing assets for longer instead of selling them outright.

This trend allows sponsors to offer more liquidity-tilted incentive structures, moving away from traditional, long-dated MIPs. Continuation and secondary vehicles typically involve shorter vesting cycles, mid-term cash incentives, and more frequent liquidity events than standard 8-10-year buyout funds.

These features better align with the expectations of today’s operating talent, who value nearer-term reward visibility along with long-term upside. These vehicles also often come with tailored performance hurdles and reset incentives. This encourages management teams to continue driving value during the extended hold period, effectively bridging the gap between traditional PE lock-ups and the more immediate payoff rhythms favored by modern professionals.

Challenges in the Current Environment

US: Ongoing debate over taxation of carried interest continues. While current law still allows for capital gains treatment (if held >3 years), the IRS has increased enforcement, and any shift in administration in 2029 could reignite reform efforts.

UK: Starting April 2026, the UK will introduce a controversial change to how Carried Interest is taxed, treating it as income and largely removing its preferential treatment. While a tax multiplier of 72.5% of qualifying carry will remain, the effective tax rate will be approximately 34.1%. This represents a notable increase from the maximum Capital Gains rate of 28% that applied until April 2025. This shift is expected to worsen the challenge for global Private Equity firms in attracting key talent to the UK, as the tax environment becomes increasingly less favorable for high earners compared to other international financial centers.

EU: The EU’s AIFMD II and various DAC6 requirements add layers of reporting complexity. Some EU jurisdictions (e.g., France, Germany) are pushing for more income-like treatment.

Global Trend: Tax authorities are increasingly focused on the actual substance of work performed vs. investment risk to justify this favorable tax treatment.

Talent Mobility and Retention

Long vesting periods and uncertain upside potential are no longer appealing to younger professionals and mobile executives who prioritize flexibility, liquidity, and quicker earnings realization. As a result, some talent is migrating to technology, venture capital, or multi-asset platforms that offer greater transparency and more immediate value.

Fundraising Pressure

As fundraising cycles elongate and LPs become more fiscally conservative, pressure on GPs to demonstrate “skin in the game” increases. This makes co-investment and carry structures both more important, but also more visible and politically sensitive.

Conclusion

Carried interest and co-investment schemes remain powerful tools, but they are no longer untouchable, static perks. PE firms must continuously revisit their reward architecture both internally and within their portfolios to reflect talent expectations, regulatory realities, and the competitive backdrop. The next evolution may not be in reworking the old, but inventing the new, embedding innovation, transparency, and flexibility into the future of incentive design.

Continue the conversation